(Bloomberg) — Stocks rallied after notching their longest weekly rally this year, as traders braced for key earnings reports from Tesla Inc. to Boeing Co. and United Parcel Service Inc.

After an unrelenting advance to all-time highs, stocks have dropped from being relatively overbought. In another sign of how greed has trumped fear, the S&P 500 hasn’t lost a rally in nearly 30 seasons. Although a month without consecutive down days may not make sense seems like a lot, the current rate is among the best since 1928, according to data compiled by SentimentTrader.

Dan Wantrobski, director of research at Janney Montgomery Scott, said: “The stock is overbought in multiple sessions and remains vulnerable to short-term profit-taking.”

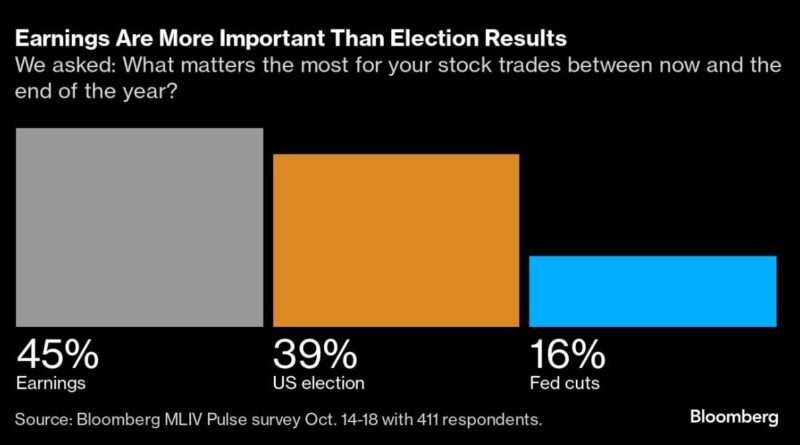

Wall Street is facing a major earnings disruption this week, with about 20% of S&P 500 companies scheduled to report. The latest Bloomberg Markets Live Pulse survey shows respondents see Corporate America’s results as more important to equity market performance than who wins the November election or policy of the Federal Reserve.

The S&P 500 was down 0.2%, with all of its major categories but tech falling. The Dow Jones industrial average fell 0.8%. Nvidia Corp. hit a record high, with the Nasdaq 100 up 0.2%. The Russell 2000 retreated 1.6%. The house builders collapsed. United Parcel Service Inc. downgraded to a sell recommendation on Barclays Plc. Boeing Co. it stopped after a temporary agreement with its union.

US 10-year yields jumped 10 basis points to 4.19%. They will test the 5% limit in the next six months amid rising inflation expectations and worries about spending, said Arif Husain of T. Rowe Price. Meanwhile, Torsten Slok at Apollo Global Management sees a high probability that the Fed will leave rates unchanged in November as the economy continues to grow.

Oil rose as China moved again to boost its economy and traders tracked supply risks from Middle East conflicts.

Volatility is high for stock options, bonds and funds alike as investors pay for protection. The risks are clear: hotly contested US elections, interest rate decisions in the US and Europe, the threat of wider conflict in the Middle East and quarterly earnings. In the stock market, sentiment is more volatile than actual volatility, and hedging against sales is preferred over trading calls.

For Matt Maley at Miller Tabak, whatever the reason, “we certainly can’t blame investors for buying protection in the bond market and/or gold.”

“With the stock market being expensive (especially in terms of buying/selling), it is more vulnerable than usual when these types of political and geopolitical issues become important concerns in the past,” he said.

Stocks lost steam after the S&P 500 posted its sixth straight week of gains. Winning streaks of that length are relatively rare, occurring just 53 times since 1950 (about 8% of all six-week periods), according to Adam Turnquist at LPL Financial.

Looking ahead, this list produced an average report of 0.2% in the following week, and 58% goes to seven times to win in seven weeks, he noted. The first six-month and 12-month returns average 5.1% and 11.4%, respectively, and both periods show the highest levels of positivity.

“While the market is entering a potentially difficult period ahead of the election and facing strong resistance near the top end of its rising price range, history suggests that investors should buy dips as performance continues after a six-week win,” he said. .

“We believe there is continued upside for stocks, especially as we enter a strong year for the markets,” said David Laut at Abound Financial. “Earnings season is on the rise and soon we will hear from the big tech companies and the latest about their use of artificial intelligence. For big tech, this is the quarter of the show -me-the-money.”

This week, Tesla is likely to face questions during its earnings call about production targets and regulatory challenges after the unveiling of its highly regarded Cybercab failed to impress investors and allay concerns about sales of the latest in cars. Boeing will have to cut back on investors who are concerned about production delays, labor disputes and dwindling cash flow.

Reports from UPS, Norfolk Southern Corp. and Southwest Airlines Co. they should reveal the combined impact of Hurricane Helene and a three-day strike by East Coast dock workers last quarter.

Jeffrey Buchbinder at LPL Financial says the range for third-quarter results is low, and analysts now only expect a 3% increase in S&P 500 earnings per share.

He said: “The low trend and supportive economic environment indicate that there is potential. “However, stocks may be the price of solid results.”

U.S. benchmark gauge companies that have beaten profit estimates so far this season have been rewarded “significantly” compared to the previous four quarters, according to Morgan Stanley strategists led by Michael Wilson . They also noted that the scope of the 2025 reforms “significantly exceeds” seasonality.

“As usual, the first few days of earnings season trigger a strong price reaction,” said Bloomberg Intelligence strategists Gina Martin Adams and Wendy Soong. “Hit and miss both result in larger than normal prices.”

Stocks that beat earnings or earnings estimates — or both — reported equivalent one-day returns to the index of 2.1%, 2.3% and 2.6%, more than double the long-term average ( for all earnings periods), they say. Mistakes also account for 3.8%, 2% and 3.7% sales, BI said.

Although the market has shown remarkable stability this year, with nine out of 10 good months, we are beginning to see a similar pattern to the 2001-2006 period when technology values were high, according to Mark Hackett Nationwide.

“Unlike the dot-com bubble, today’s leading technology firms have solid fundamentals, but the market is far from ‘normal,'” he said. “High expectations are a warning sign for potential volatility in the next few years. Investors should be prepared to limit returns and volatility, especially as cracks begin to appear beyond 2024 .”

US stocks are unlikely to maintain their peak performance of the past decade as investors turn to other assets including bonds for better returns, according to Goldman Sachs Group Inc. strategists including David Kostin.

They said the S&P 500 is expected to post an average annual return of just 3% over the next 10 years. That compares to 13% a decade ago, and a long-term average of 11%.

The group wrote in the letter of Oct. 18: “Investors should prepare for equity returns in the next ten years that are close to providing normal performance.”

Company Highlights:

-

SAP SE said its cloud revenue grew 25% in the third quarter, as Europe’s biggest software company pushes customers away from legacy systems installed on-premises.

-

Qualcomm Inc. introduced a more powerful processor designed to bring laptop-level capabilities to smartphones, helping devices take advantage of new artificial intelligence tools.

-

Microsoft Corp. is launching a suite of artificial intelligence tools designed to send emails, manage records and take other steps on behalf of business employees, boosting AI performance that is boosting competition with competitors such as Salesforce Inc.

-

Spirit Airlines Inc. it rose after the carrier got more time to deal with a heavy debt that raised expectations of a recession.

-

Kenvue Inc. became independent after rival trader Starboard Value took a stake in the maker of Tylenol with an eye to making changes to raise the company’s stock price.

Highlights this week:

-

Christine Lagarde of the ECB is interviewed by Bloomberg Television, Tuesday

-

The BOE’s Andrew Bailey along with the ECB’s Klaas Knot and Robert Holzmann will speak at the Bloomberg Global Regulatory Forum in New York on Tuesday.

-

Philadelphia Fed President Patrick Harker speaks, Tuesday

-

Canadian rate decision, Wednesday

-

Eurozone consumer confidence, Wednesday

-

US real estate sales, Wednesday

-

Boeing, Tesla, Deutsche Bank earnings, Wednesday

-

Fed’s Beige Book, Wednesday

-

US new home sales, jobless claims, S&P Global Manufacturing and Services PMI, Thursday

-

UPS, Barclays earnings, Thursday

-

The Fed’s Beth Hammack speaks, Thursday

-

US durable goods, University of Michigan consumer sentiment, Friday

Some of the main movements in the markets:

Stocks

-

The S&P 500 was down 0.2% as of 4 pm in New York

-

The Nasdaq 100 rose 0.2%

-

The Dow Jones industrial average fell 0.8%

-

MSCI World Index fell 0.4%

-

Russell 2000 Index down 1.6%

Finances

-

The Bloomberg Dollar Spot Index rose 0.4%

-

The euro fell 0.5% to $1.0815

-

The British pound fell 0.5% to $1.2983

-

The Japanese yen fell 0.8% to 150.79 per dollar

Financial statements

-

Bitcoin is down 1.5% at $67,746.88

-

Ether is down 1.2% at $2,679.24

Obligations

-

The 10-year Treasury yield advanced 10 basis points to 4.19%

-

German 10-year yields advanced 10 basis points to 2.28%

-

Britain’s 10-year yield advanced eight basis points to 4.14%

Goods

This story was produced with the help of Bloomberg Automation.

–Courtesy of Vildana Hajric.

Best Reads from Bloomberg Businessweek

©2024 Bloomberg LP